It’s been a while since I last did an update of the blog again as I recently joined another firm which keeps me busy, and I was restricted to make too much exposure on the blogging front due to the nature of my role.

In any case, I just wanted to take this opportunity to refresh my spreadsheet model on the intrinsic value calculation on some of the core China related companies that I own, which also has recently been the topic of the chat throughout the media because of the stimulus announcement that was announced.

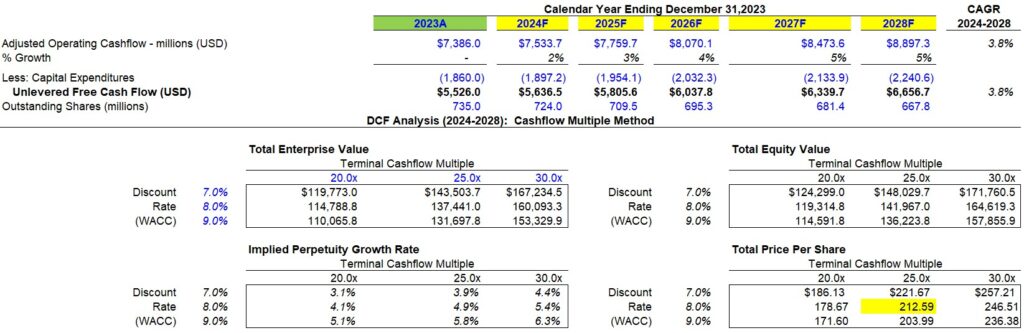

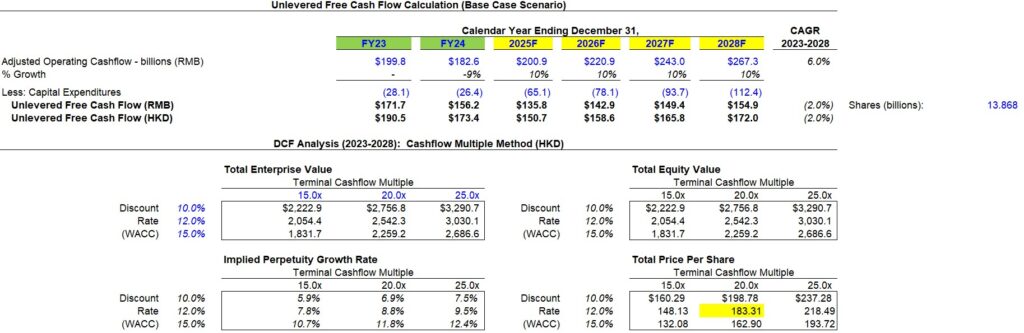

Alibaba Holdings – Intrinsic Value Calculation

I updated my spreadsheet to reflect the latest FY23 and FY24 numbers, and made two major changes to the model.

First, I took out the capex front of the Alibaba Cloud Infrastructure which the company is investing for AI for growth as the huge drop in Q1 FCF was due to that. It will be hard to quantify the future benefits of such investment without doing any deep dive but at this moment, we simply just do not have enough information to do that. Without that component, I am projecting for an organic increase in 10% FCF otherwise during the year.

The second piece which I updated was its shares outstanding which the company has done major share buyback since its announcement a couple of quarters ago, and I projected for the shares outstanding to decline by 10% each year until 2028.

The model returned me an intrinsic value calculation of HKD 183.31.

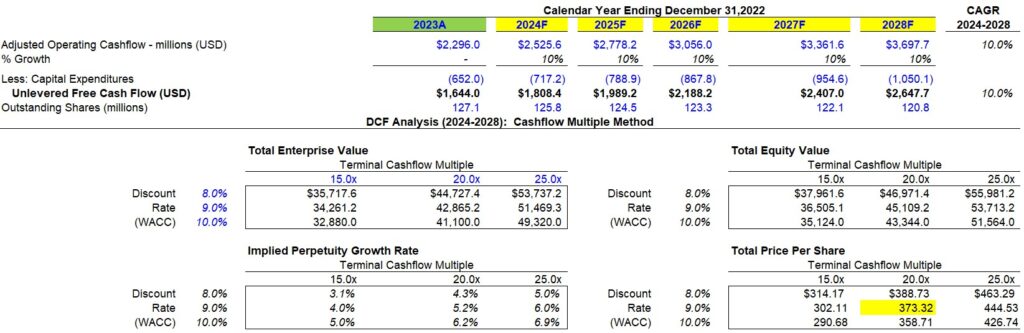

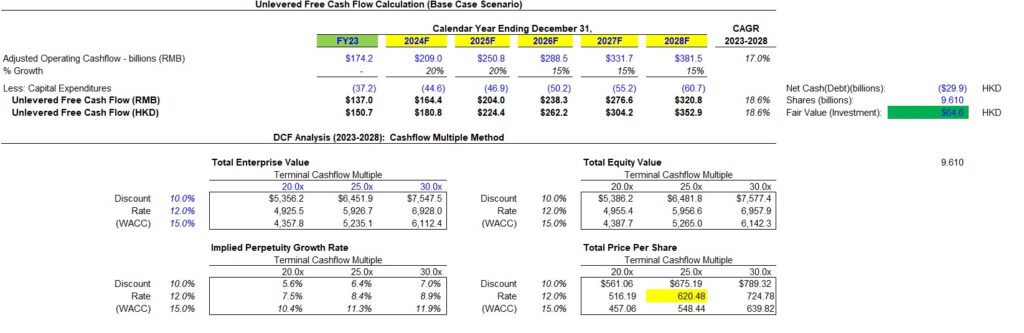

Tencent Holdings – Intrinsic Value Calculation

For years, Tencent has a habit of spending and reinvesting their free cash flow into new businesses and do not maintain a huge chunk of cash on their balance sheet. Recently, they even announced that they will be doubling the share repurchase buyback, which will improve their EPS over time.

These businesses are recorded as part of their equity share of profits and not into the organic model of their operating cashflow so we’ll have to add that in at the end of the day.

As of Q2 FY2024 latest result announcement, the Fair Value of the shareholdings in listed investee companies, excluding subsidiaries, stand at RMB 564.5 billion, which is more than half trimmed down from what it used to be RMB 1.36 trillion around 3 years back. Investors of Tencent might have recalled that they have given out the likes of Meituan and JD shares as special dividend in specie over the years. For RMB 564.5 billion, if we convert it into HKD/share, it is approximately worth HKD64.6 (RMB 564.5 billion x 1.1 HKD / 9.61 billion outstanding shares).

For its operating business, I am projecting a return to organic recovery case scenario which embeds a model of 20% growth for the next 2 years, then 15% for the next 3 years. For the first half of FY24, we are already seeing that moving into reality.

Cashflow multiple of 25x is used for high quality companies growing at the higher end, which I think companies like Tencent fits the bill.

The intrinsic value I get from the model is HKD 620.48. Combining it with the HKD64.6 investment fair value, we get a total intrinsic value for Tencent of about HKD 685.

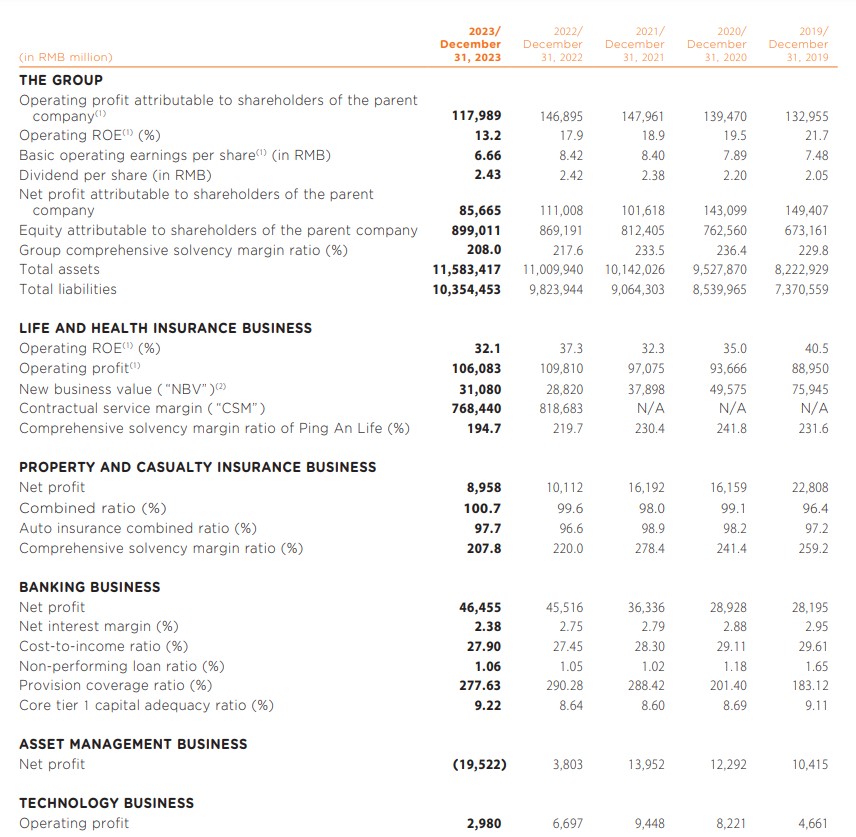

Ping An – Intrinsic Value

There are 3 things that stand out to me for Ping An in FY2023.

First, the property market totally wrecked the entire China and affected insurance and banks with exposure to property companies like Ping An Insurance. Provision for impairment has gone up and solvency ratio has also gone up. Net profit for its property and casualty insurance segment has plunged to just under RMB 9 billion. Non-performing loans rose up to 1.22.

This should recover well into FY2024 now that they have kitchen-sink the worst scenario and this asset management segment should recover by at least RMB20 billion into FY2024.

Next, the Life and Health insurance business has recovered well and look to trajectory growth back in FY24 after the company putting in efforts in the past few years the number of retail customers and agent per customer ratio served.

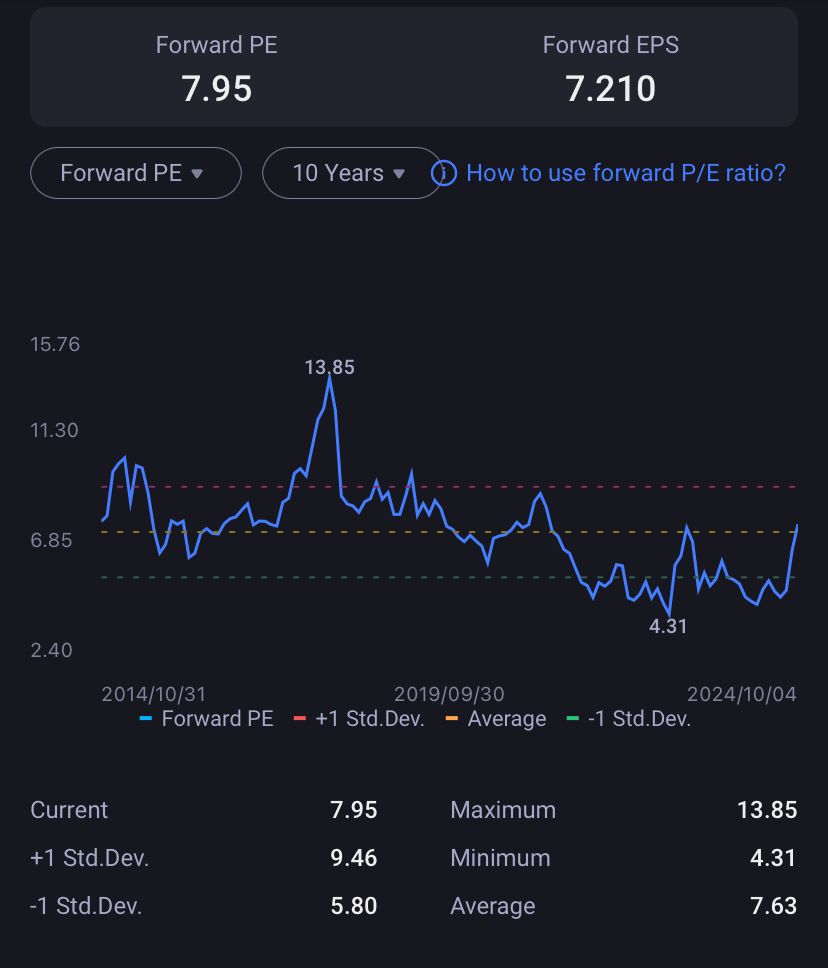

For FY24, I do expect the company to return to its RMB8 EPS at a forward PE Ratio of around 8x. This will put the company at a share price expectation of around RMB 64 or HKD 70.8.

If the company can expect further growth to commence, we can even plug in further PE expansion to +1 SD deviation which will put the intrinsic value even higher.

3 Ways to Play the China Market

There are 3 ways to play the China market for those who are somewhat keen in getting back into this market.

First, you can directly buy into your position when market opens next week. This will give you a direct exposure to ride the upside (and also downside) if there’s any.

Second, since the trend seems to be heading into strength, you can write a put option for these shares, as they may continue their way higher when market opens next week. If market declines into correction, you can also keep your premium and obtain your shares at your desired lower prices.

Third, If you are already having a position, you can write a covered call for these positions at the intrinsic value strike price mentioned above. The premium is juicy since it’s been pushed up quite a bit over the last week and you might get additional premium in return.

With many companies looking at the resistance, and with China market going to reopen next week, it will be a bull vs bear fight and another one to watch for next week.